High-Capacitance MLCCs Are Up 400% and Sold Out — What's Really Happening, and What Comes Next

Industry channel checks paint a stark picture: AI server demand has broken the MLCC market in a way not seen since 2018 — and this time, the shortage may run deeper.

SOURCING & SUPPLY CHAIN

JoeZ

7/3/20264 min read

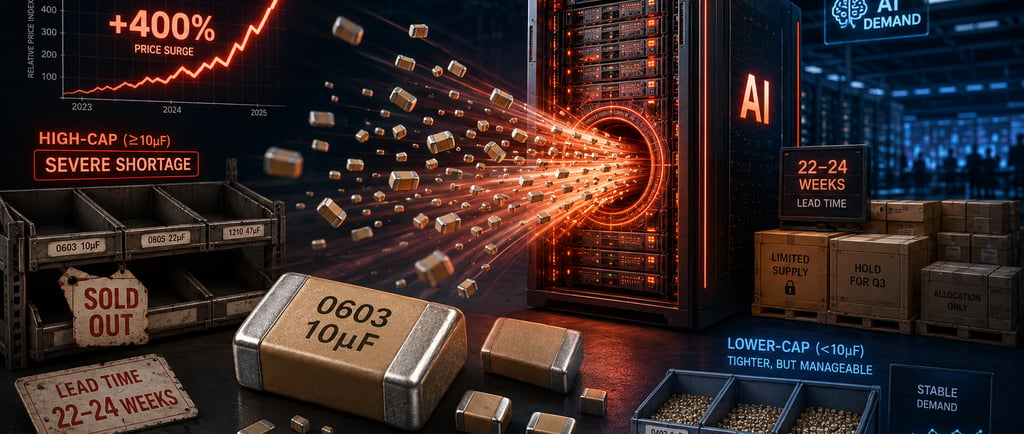

If you've tried to buy high-capacitance MLCCs on the spot market recently, you already know something is wrong. The benchmark 0603 10µF (106) part has climbed from roughly ¥17/K at the start of the year to ¥80–90/K today — an increase of around 400% in six months. Lead times from original manufacturers have stretched from 18–20 weeks to 22–24 weeks and are still moving out. Traders are sitting on an estimated six months of inventory and refusing to sell.

And according to supply-chain sources, this is only the middle of the story. As long as AI orders hold, spot prices on high-cap parts could reach roughly 10x year-start levels by year end — with some in the industry expecting next year's peak to exceed the 12–15x spike of the 2018 shortage.

Here's what the data shows, and what it means if you're building hardware right now.

One Market, Two Very Different Stories

The first thing to understand about this cycle: "MLCC shortage" is too broad a phrase. The market has split into two distinct scripts.

High-capacitance parts are in genuine structural shortage. AI servers consume a disproportionate share of high-cap MLCCs, only a handful of manufacturers worldwide can produce them, and the overflow orders spilling out of the Japanese majors have already been absorbed. There is simply no slack left. Industry consensus puts the earliest meaningful relief in Q3–Q4 of next year.

Mid- and low-capacitance parts are tight, but not broken. Chinese manufacturers have expanded capacity aggressively since 2021, so the squeeze is far milder than 2018. The standout exception is the 0603 100nF (104) line — the fastest-rising part in the low/mid-cap segment, up from ¥7–9/K to around ¥30/K. But most observers expect low/mid-cap pressure to ease around October as consumer demand visibility improves.

If your BOM leans on high-cap parts, you're in the hard script. If it doesn't, you have more room — but not immunity, because capacity displacement is spreading the pain.

Why AI Broke the Market: 480,000 Capacitors Per Rack

The demand mix for MLCCs has been fundamentally re-drawn. AI now accounts for close to 30% of total MLCC demand, with automotive at roughly 20%, solar/storage/power at another 20%, and consumer electronics at about 30%. Within the high-capacitance segment specifically, AI's share rises to 30–40%.

The per-unit numbers explain why. A single accelerator board in the H100 era used 1,500–1,800 MLCCs. On GB200/GB300 platforms, that figure is approximately 3,000. A full GB300 rack consumes around 450,000 MLCCs; the next-generation architecture pushes that to roughly 480,000 per rack — and the count is still climbing.

Faced with this, Japanese manufacturers have begun actively triaging their customer base: trimming consumer-electronics allocations and redirecting capacity toward AI servers, power supplies, and automotive-grade parts. Everyone else, watching their lead times slip, has responded by overbooking to lock in supply early — which is exactly the behavior that pushed high-cap lead times from 18–20 weeks to 22–24 weeks, and dragged some mainstream low/mid-cap parts past 16 weeks.

Where the Inventory Actually Is (Hint: Not With the Manufacturers)

Inventory distribution across the channel is severely lopsided, and it explains the spot-market pricing you're seeing:

The original manufacturers and authorized distributors are essentially dry. End factories are carrying one to two months of stock at most. The real inventory sits at the very end of the chain — with independent traders holding roughly six months of high-cap stock and three to four months of low/mid-cap, buying but not selling, and by most accounts planning to sit on it for several more months waiting for prices to climb further.

The pricing cascade is straightforward. Manufacturers have raised distributor pricing by roughly 30–50%; distributors add another 15–20% on the way out. Traders, who sit outside any manufacturer price control, are quoting at 3–5x. Large customers with supply-assurance agreements can still squeeze out their allocations. Small and mid-sized buyers — who get no capacity allocation — are pushed into the spot market at whatever price the traders name. That's the origin of the distorted pricing on certain part numbers.

The Increases Are Moving From Spot to Contract — and the Calendar Runs Through Mid-2027

What started as spot-market chaos is now being formalized into contract pricing. Overseas manufacturers are expected to issue official price-increase letters in July–August: 20–30% on consumer high-cap parts, at least 15% on low/mid-cap.

The manufacturer roadmap from there is remarkably explicit:

Q3 2026: contract prices up another 10–20%

Q4 2026: a further ~20% if order volumes hold

H1 2027: an additional ~30% of headroom expected

One market rumor captures the strategic logic: Samsung Electro-Mechanics is reported to have signed a long-term AI-server agreement with a major cloud provider covering the flagship 107 series at roughly ¥1.2–1.5 per piece, on non-cancellable terms. The pattern: lock in AI hyperscalers at modest 10–20% increases to guarantee volume, then recover margin from everyone else — other customers and the distribution channel. In other words, these price increases are really a customer-selection mechanism.

And the supply side isn't riding to the rescue. Major manufacturers are planning capacity expansions of only 10–20%, and the equipment needed for those expansions now carries lead times approaching 12 months — meaning no meaningful new supply in the short term. Chinese manufacturers, prioritizing market-share gains, are following the price increases only cautiously.

What This Means If You're Building Hardware

For hardware startups and small-to-mid-sized manufacturers — the buyers with no allocation leverage — this cycle demands action, not observation:

Audit your BOM for high-cap exposure now. Identify every high-capacitance MLCC on your designs and quantify your exposure. These are the parts where relief is a year or more away.

Design around the bottleneck where you can. For new designs and revisions, evaluate whether high-cap positions can be split into parallel lower-capacitance parts, moved to alternative dielectrics or packages, or sourced from qualified domestic Chinese manufacturers whose pricing has stayed comparatively restrained.

Lock coverage before the July–August price letters land. Contract pricing has a published escalation calendar through mid-2027. Inventory bought at today's distributor pricing — painful as it looks — may be cheaper than anything available in Q4.

Be disciplined about spot purchases. Trader-held inventory at 3–5x is where pricing is most distorted. Buy there only for genuine line-down risk, verify authenticity rigorously, and never let spot pricing anchor your long-term cost model.

Use your manufacturing partner's aggregated demand. One advantage of working with an EMS partner is consolidated purchasing volume and established distributor relationships — which matters most in exactly this kind of market, when allocation goes to whoever the channel already knows.

The 2018 MLCC shortage taught the industry that these cycles reward the prepared and punish the reactive. This one looks set to teach the same lesson, at larger scale.

SERVICES

Peakingtech © 2025. · Shenzhen, China · Privacy Policy · Terms of Service

Contact Form

Metal Parts

Peakingtech® is a registered trademark of Peakingtech Co in the United States.

COMPANY

CONTACT