The Shift in Global Manufacturing Exports: A Deep Dive into the Rise of China and the Decline of Traditional Powerhouses

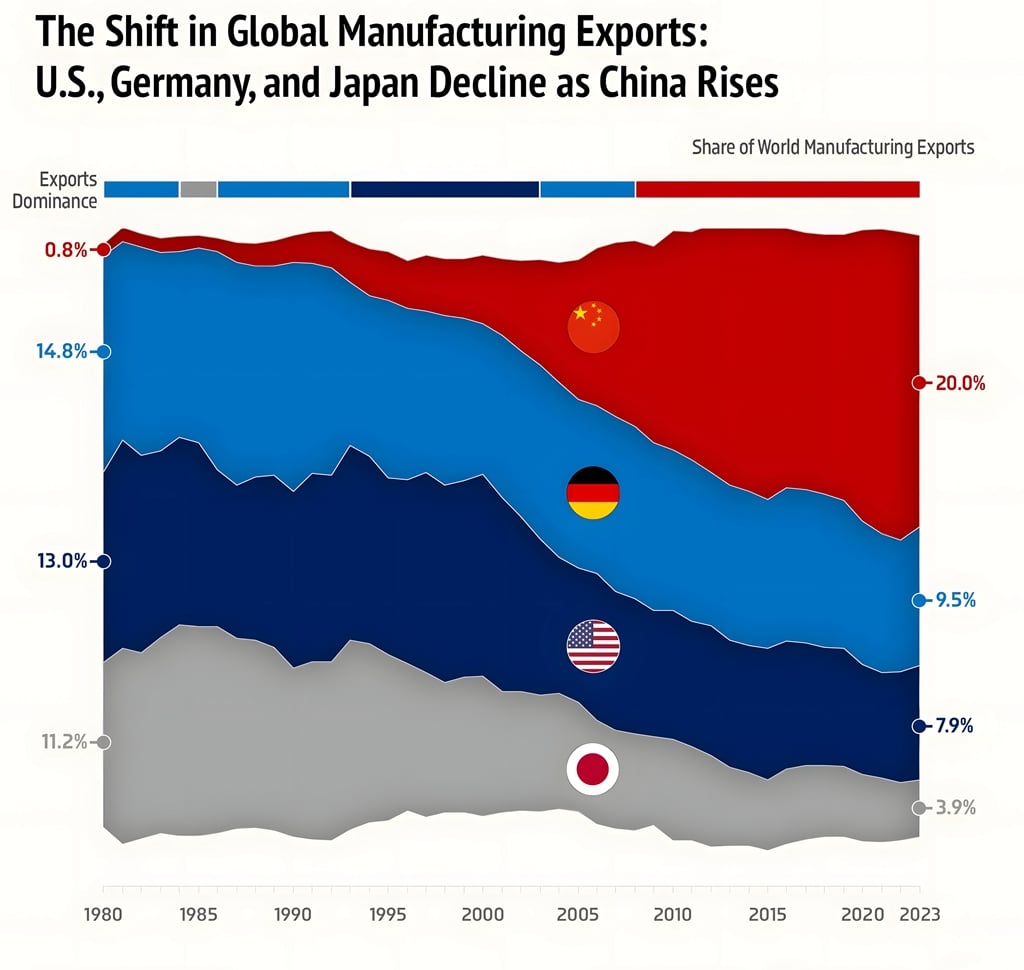

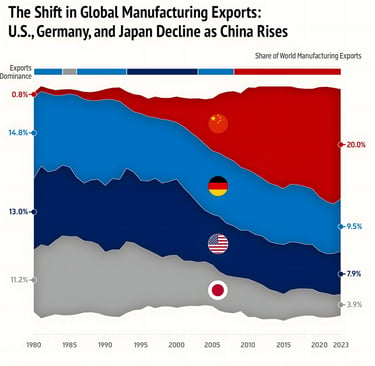

The global manufacturing landscape has undergone a seismic shift over the past four decades, as illustrated by a striking infographic from Econovisuals, sourced from the World Trade Organization (WTO).

SOURCING & SUPPLY CHAIN

4/1/20255 min read

The global manufacturing landscape has undergone a seismic shift over the past four decades, as illustrated by a striking infographic from Econovisuals, sourced from the World Trade Organization (WTO). The chart, titled "The Shift in Global Manufacturing Exports: U.S., Germany, and Japan Decline as China Rises," visually captures the dramatic reconfiguration of manufacturing export dominance from 1980 to 2023. This transformation has profound implications for global trade, economic policies, and geopolitical dynamics—especially in light of recent tariff wars initiated by former U.S. President Donald Trump and their potential continuation under future administrations. In this article, we’ll explore the trends depicted in the infographic, analyze the underlying factors driving these changes, and forecast the future of global manufacturing in the context of ongoing trade tensions.

The Decline of Traditional Manufacturing Giants

In 1980, the United States, Germany, and Japan were the undisputed leaders in global manufacturing exports. According to the infographic, the U.S. held a 14.8% share of world manufacturing exports, Germany 13.0%, and Japan 11.2%. Together, these three nations accounted for a significant portion of global manufacturing output, reflecting their industrial prowess, technological innovation, and established trade networks. This dominance was built on decades of post-World War II economic growth, with the U.S. benefiting from its vast industrial base, Germany from its engineering excellence, and Japan from its rapid industrialization and focus on high-quality electronics and automobiles.

However, by 2023, the landscape had shifted dramatically. The U.S. share of global manufacturing exports had fallen to 9.5%, Germany’s to 7.9%, and Japan’s to a mere 3.9%. This decline reflects a combination of factors, including rising labor costs in these developed economies, the offshoring of manufacturing to lower-cost regions, and the inability to compete with the scale and efficiency of emerging manufacturing powerhouses—most notably, China.

The Rise of China: A Manufacturing Juggernaut

The most striking feature of the infographic is the meteoric rise of China, which went from a negligible 0.8% share of global manufacturing exports in 1980 to a commanding 20.0% by 2023. This ascent began in earnest after China’s economic reforms under Deng Xiaoping in the late 1970s and accelerated following its entry into the WTO in 2001. China’s manufacturing boom was fueled by several key factors:

Low Labor Costs: In the 1980s and 1990s, China offered an abundant supply of low-cost labor, making it an attractive destination for multinational corporations looking to reduce production costs.

Government Support: The Chinese government implemented policies to support industrial growth, including subsidies, tax incentives, and the development of special economic zones (SEZs) that encouraged foreign investment and export-oriented manufacturing.

Scale and Infrastructure: China invested heavily in infrastructure, such as ports, railways, and factories, enabling it to scale production rapidly and efficiently. The country also developed a robust supply chain ecosystem, making it a one-stop shop for manufacturing needs.

Globalization and Trade Liberalization: The liberalization of global trade in the 1990s and 2000s allowed China to integrate into global supply chains, exporting everything from textiles and toys to electronics and machinery.

By the 2010s, China had solidified its position as the "world’s factory," producing a vast array of goods at competitive prices. Its dominance in manufacturing exports has reshaped global trade patterns, with many countries becoming heavily reliant on Chinese goods.

The Impact of Tariff Wars: Trump’s Trade Policies and Beyond

The rise of China as a manufacturing superpower has not gone unchallenged. During his presidency (2017–2021), Donald Trump initiated a series of trade policies aimed at reducing the U.S. trade deficit with China and revitalizing American manufacturing. These policies included imposing tariffs on Chinese goods, ranging from 10% to 25%, on products like steel, aluminum, and consumer electronics. Trump’s rationale was twofold: to protect domestic industries from what he described as unfair trade practices (such as intellectual property theft and currency manipulation) and to encourage companies to bring manufacturing back to the U.S.

The tariff war had mixed results. On one hand, it disrupted global supply chains, forcing some companies to diversify their manufacturing bases away from China. Countries like Vietnam, India, and Mexico saw an uptick in manufacturing activity as businesses sought to mitigate the risks of tariffs. On the other hand, the tariffs increased costs for American consumers and businesses, as many U.S. companies passed on the higher costs of imported goods. Moreover, China retaliated with its own tariffs on U.S. goods, particularly agricultural products like soybeans, hurting American exporters.

As of March 31, 2025, the tariff war’s legacy continues to shape global trade dynamics. While President Joe Biden initially retained many of Trump’s tariffs, his administration has focused on a more multilateral approach, working with allies to address China’s trade practices. However, with Trump’s potential return to the presidency in 2025 (following the 2024 election), there is speculation that he might double down on his protectionist policies, possibly introducing even higher tariffs or expanding them to other countries.

Forecasting the Future of Global Manufacturing

Looking ahead, the global manufacturing landscape is likely to be shaped by several key trends, particularly in the context of ongoing trade tensions:

Reshoring and Nearshoring: The tariff wars and the disruptions caused by the COVID-19 pandemic have highlighted the risks of over-reliance on China for manufacturing. Many companies are now exploring reshoring (bringing production back to their home countries) or nearshoring (moving production to nearby countries). For the U.S., this could mean increased manufacturing in Mexico or Canada, while European countries might look to Eastern Europe or North Africa. However, reshoring is expensive due to higher labor costs in developed economies, and it remains to be seen whether government incentives can offset these costs.

China’s Continued Dominance: Despite the tariff wars, China is unlikely to cede its position as the world’s leading manufacturing exporter anytime soon. The country has been moving up the value chain, focusing on high-tech industries like semiconductors, electric vehicles, and renewable energy. Initiatives like "Made in China 2025" aim to make China a leader in advanced manufacturing, reducing its reliance on low-cost labor and increasing its technological edge.

Emerging Players: As China’s labor costs rise and geopolitical tensions persist, other countries are stepping into the manufacturing space. India, with its large workforce and government-led initiatives like "Make in India," is positioning itself as an alternative to China. Southeast Asian nations like Vietnam and Thailand are also becoming manufacturing hubs, particularly for electronics and textiles.

Impact of Tariffs and Trade Policies: If Trump or a similarly protectionist administration escalates the tariff war, we could see further fragmentation of global supply chains. Higher tariffs might encourage more reshoring to the U.S., but they could also lead to higher inflation and strained relations with trading partners. Conversely, a more collaborative approach—such as negotiating trade agreements that address issues like intellectual property and labor standards—could stabilize global trade while still addressing concerns about China’s practices.

Technological Disruption: Advances in automation, artificial intelligence, and 3D printing are transforming manufacturing. These technologies could reduce the importance of low-cost labor, potentially leveling the playing field for developed economies like the U.S., Germany, and Japan. However, China is also investing heavily in these technologies, which could further solidify its dominance.

Conclusion

The infographic from Econovisuals paints a clear picture of the dramatic shift in global manufacturing exports over the past four decades. The decline of the U.S., Germany, and Japan, coupled with the rise of China, reflects the broader forces of globalization, economic policy, and technological change. While tariff wars and protectionist policies have introduced new uncertainties, they have also spurred a reevaluation of global supply chains, with potential opportunities for emerging manufacturing hubs.

As we move into the late 2020s, the global manufacturing landscape will likely remain in flux. China’s dominance is secure for now, but its position could be challenged by rising costs, geopolitical tensions, and technological disruptions. For traditional manufacturing powers like the U.S., Germany, and Japan, the path forward involves embracing innovation, investing in advanced manufacturing, and navigating the complexities of global trade policies. The tariff wars initiated by Trump have set the stage for a new era of economic competition—one that will require careful balancing of national interests with the realities of a deeply interconnected global economy.

SERVICES

Peakingtech © 2025. · Shenzhen, China · Privacy Policy · Terms of Service

Contact Form

Metal Parts

Peakingtech® is a registered trademark of Peakingtech Co in the United States.

COMPANY

CONTACT