Navigating the 2025 Tariff Shock: Strategies for a Resilient Electronics Supply Chain

Learn how electronics manufacturers can build a resilient supply chain across China, India, and emerging markets in 2025. Explore strategies to offset U.S. tariffs, leverage India’s PLI incentives, diversify production, and safeguard against geopolitical and currency risks.

SOURCING & SUPPLY CHAIN

JoeZ

8/11/20254 min read

Executive Summary

The global electronics industry is facing acute stress from unexpected geopolitical developments. In 2025, U.S. tariffs on Indian non-smartphone electronics were raised to 50 percent, sharply undermining India's growing export base, particularly in inverters, battery chargers, and transformer parts. Meanwhile, major players like Apple and Samsung have secured exemptions, underscoring widening disparities in exposure across the sector. To equip your enterprise for the turbulent ahead, this article provides strategic guidance on:

Balancing production between China, India, and alternative regions

Leveraging India’s domestic incentives, such as the Production-Linked Incentive (PLI) program

Diversifying supply chain geography to de-risk trade exposure

Strengthening resilience through policy foresight and multi-source flexibility

Using financial instruments and procurement strategies to hedge tariff and currency risks

The Tariff Shock: What Changed and Why It Matters

1.1 Tariffs Reach 50% on Indian Non-Smartphone Electronics

In early August 2025, U.S. President Trump doubled tariffs on Indian non-smartphone electronics to 50 percent, largely in response to India's continued purchase of Russian oil. Smartphone exports, which comprised 72 percent of India’s $14.6 billion electronics exports to the U.S., largely obtained exemptions. Nonetheless, the value chain for ancillary manufacturers—producing inverters, chargers, and transformer parts—is severely disrupted.

1.2 Electronics Sector Under Pressure

The knock-on effects of soaring tariffs have already begun to crackle through valuations and export viability, placing non-smartphone manufacturers in a precarious position.

1.3 Macroeconomic Ripples

Moody’s warns the tariffs may reduce India’s fiscal-year GDP growth by 0.3 percentage points, supporting a projected 6.3% baseline.

Rupee volatility is on the rise, weighed down by foreign portfolio outflows and investor uncertainty.

1.4 Escalating Trade Tensions

Trade talks are currently stalled: President Trump has halted further negotiations with India until tariff disputes are resolved TIME. Meanwhile, sectors such as electronics, textiles, and auto components are abundant targets—some estimates put total exposed exports at 30–31 billion USD.

2. Strategic Objectives for Project Leaders

2.1 Enhance Supply Chain Resilience

Diversify geography to avoid concentration risk.

Design flexibility to shift production across multiple regions on short notice.

Build buffers—inventory, local sourcing—to soften sudden tariff shocks.

2.2 Optimize Cost Structures Amid Tariffs

Reassess total landed costs, including tariff burdens, logistics, and FX implications.

Seek PLI zones and other local incentives to offset higher cost exposure.

2.3 Drive Long-Term Sustainability

Future-proof capacities in promising regions.

Foster innovation and local partnerships to reduce supply dependence on geopolitically unstable regions.

3. India vs. China: Pros, Cons, and Nuances

3.1 India: A Dual-Edged Sword

Strengths:

Fastest-growing smartphone export hub; Apple, Samsung, and others invest in PLI-linked facilities.

Strong domestic programs: Production-Linked Incentives (PLI), SEZs, Special Economic Zones, EHTPs; government funding to attract electronics FDI.

Weaknesses:

New 50% tariffs hit non-smartphone electronics hard.

Execution risks, regulatory complexity, and currency instability add uncertainty.

3.2 China: Maturity With Increasing Risk

Strengths:

World-class infrastructure, mature procurement networks, and scale efficiencies.

Weaknesses:

Trade tensions and tariff exposure remain high.

Political volatility and global push for “China-plus-one” strategies are steering companies to other regions.

3.3 Other Regions Gaining Ground

Southeast Asia (e.g., Vietnam): RCEP member, lower tariffs, growing electronics footprint AInvest.

Eastern Europe (e.g., Poland, Hungary): EU-centric, strong in manufacturing/logistics, attractive for diversification.

4. Supply Chain Blueprint for Electronics Decision-Makers

4.1 Dual-Hub Strategy: India + Secondary Region

Lead Manufacturing Node: India—leveraging PLI zones for smartphones and connected electronics.

Fallback/Adjunct Node: Vietnam or Eastern Europe—positioning to shift production of tariff-sensitive components as needed.

4.2 Component Segmentation for Flexibility

Smartphones and high-value products: India, with exemptions buffering tariff exposure.

Auxiliary electronics (chargers, inverters, transformer parts): Diversify to Vietnam, Mexico, or Eastern Europe to sidestep 50% tariffs.

4.3 Structural Partnerships

Forge JV or procurement alliances with Indian contract manufacturers looking to expand globally.

Link with Vietnamese or Polish manufacturing hubs for agility.

4.4 Financial Hedging Strategies

Hedge currency exposures (e.g., INR volatility) with forward/futures contracts.

Use transfer pricing and incoterms strategically to minimize tariff basin charges.

4.5 Inventory and Logistics Resilience

Build strategic inventory buffers in tariff-safe jurisdictions.

Opt for dual logistics routes, such as routing components via UAE or Netherlands to balance supply chain risks.

4.6 Advocacy and Policy Engagement

Monitor U.S.–India trade developments closely. Tariff exemptions and FTA negotiations could shift thresholds rapidly.

Align with trade associations to push for negotiations, relief programs, or bilateral agreements.

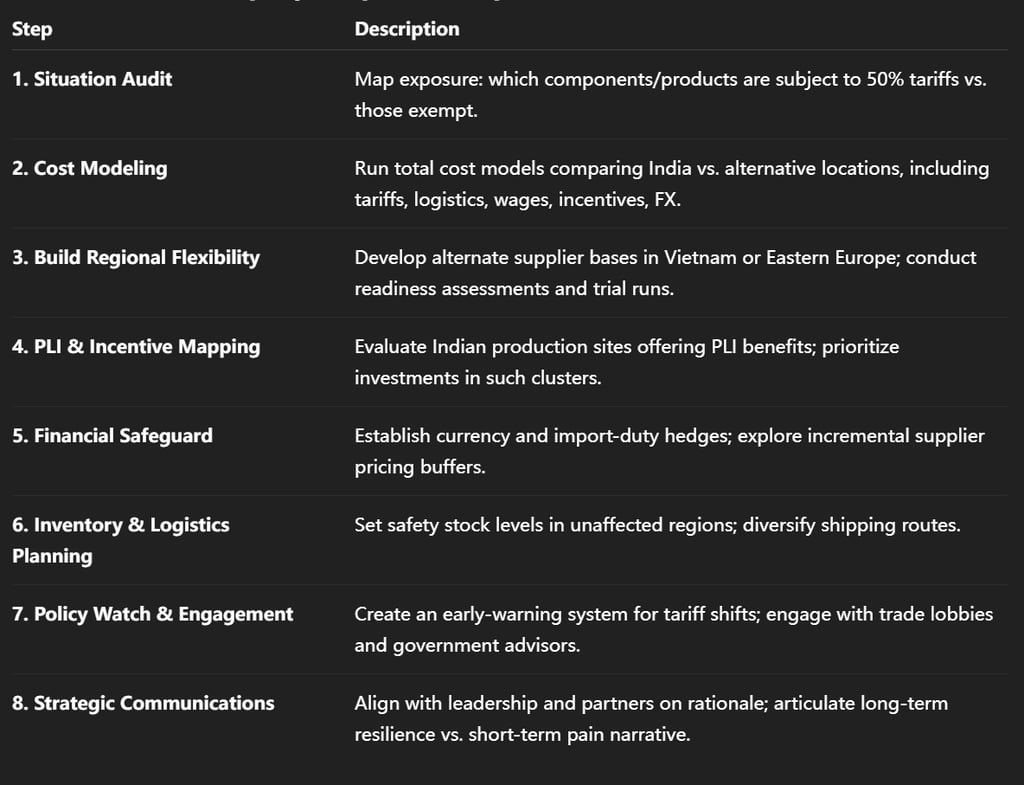

5. Action Plan: Step-by-Step Roadmap

Real-World Precedents in Supply Chain Adaptation

Apple shifted iPhone production to India, initially building capacity well before tariffs intensified. This foresight allowed it to skirt punitive duties and tap PLI advantages; its India output is expected to double by 2025.

Indian contract manufacturers are now aggressively pursuing global expansion—through M&A and partnerships—to leverage tariff-driven opportunities, even as ROI concerns linger.

Domestic resilience: Despite Q3 2025 reporting 36% QoQ growth in non-smartphone electronics exports ($4.8 billion), further scaling now faces headwinds from new tariffs.

Beyond India: The Geography of Diversification

Southeast Asia (Vietnam)

RCEP membership facilitates lower tariff regimes.

Electronics manufacturing base is expanding rapidly.

Provides strategic redundancy against Indian export risks.

Eastern Europe (Poland, Hungary, Czech Republic)

Gaining investment via EU recovery funds (~€135 billion in Poland), especially in green energy and advanced manufacturing.

Offers near-shore proximity to EU and North America, improving lead times and political safety.

Regulatory & Logistics Edge

Comparative advantage in FTA regimes, customs ease, and geopolitical alignment—especially for goods destined for the U.S., EU, or the Middle East.

Risks and Challenges to Navigate

Tariff Volatility

U.S. trade policy can change abruptly, as shown by the sudden 50% tariff increase

Execution Complexity

Scaling in India requires navigating labor regulations, infrastructure limitations, and local governance.

Simultaneously standing up facilities in other regions requires significant CAPEX and supply chain coherence.

Local Incentive Reliance

PLI and other incentives are time-bound and often performance-tied; uninterrupted execution is critical to secure benefits.

Currency Swings

INR volatility (≈8% depreciation already) adds FX risk for cost planning and financial performance.

Conclusion: Building Supply Chain Preparedness for the Future

For electronics project executives, the 2025 tariff escalation underscores a pivotal shift from “efficiency-first” to “resilience-first” supply chains. India remains a promising hub—especially for smartphone and high-value electronics under PLI—but the 50% tariffs on non-smartphone goods mandate a strategic rethink.

Your blueprint forward:

Leverage India for core, tariff-protected segments and scale through PLI zones.

Diversify geographically: Prepare Vietnam or Eastern Europe as alternate supply hubs.

Segment products smartly: Allocate tariff-sensitive components to low-duty regions.

Use financial tools to hedge tariff and FX risks.

Stay policy-savvy, agile, and ready to pivot quickly.

The next decade will reward companies that rethink supply chains not just for cost—but for geopolitical flexibility, strategic autonomy, and resilience. This moment is not just a crisis—it’s an inflection point. Those who act decisively may well emerge stronger.

SERVICES

Peakingtech © 2025. · Shenzhen, China · Privacy Policy · Terms of Service

Contact Form

Metal Parts

Peakingtech® is a registered trademark of Peakingtech Co in the United States.

COMPANY

CONTACT